Savings on energy bills this winter as price cap falls

- The level of the price cap will fall by £84 from October to its lowest level £1,042, driven by lower wholesale energy costs following COVID-19

- The level of the cap for prepayment meter customers will fall by £95

- Ofgem recommends the price cap remains in place in 2021 which would ensure that 15 million households continue to pay a fair price for their energy.

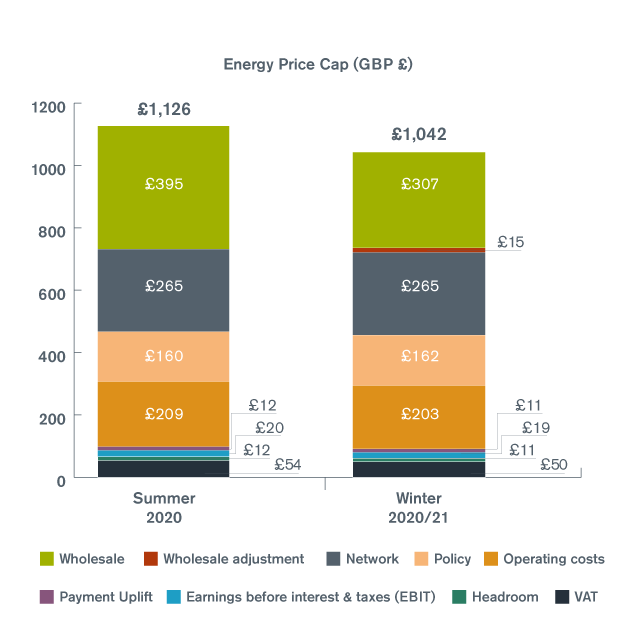

The price cap will fall by £84 from £1,126 to £1,042 per year for the winter period (October-March). This is the lowest level of the cap since it was introduced on January 1 2019.

The level of the cap for pre-payment meter customers will fall by £95 from £1,164 to £1,070 per year for the same six month period. (see notes)

The changes mean that around 11 million households on default tariffs and 4 million on prepayment meters (around half the population in total) will enjoy significant savings on their energy bills this winter.

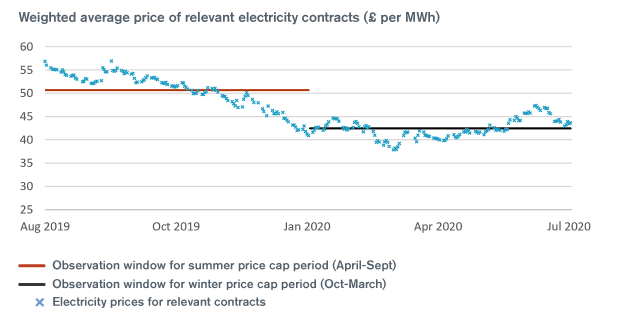

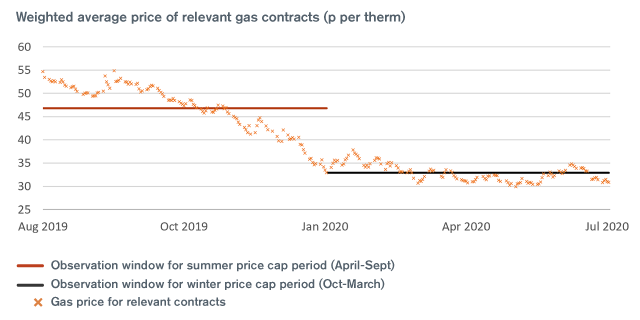

The reduction is due to a sharp decrease in wholesale gas prices since the cap was last updated in February.

The COVID-19 crisis has depressed energy demand although wholesale gas prices have started to recover since hitting 20 year lows in the spring.

If wholesale energy prices continue to rise over the coming months, the cap is likely to rise in April to reflect these higher costs.

Ofgem adjusts the level of the cap twice a year to reflect the estimated costs of supplying electricity and gas to homes for the next six-month period.

Suppliers cannot charge customers who do not switch and are on default deals more than the level of the cap, although they can charge less.

This ensures that these customers pay a fairer price for their energy.

Jonathan Brearley, chief executive of Ofgem, said: “Millions of households, many of whom face financial hardship due to the COVID-19 crisis, will see big savings on their energy bills this winter when the level of the cap is reduced.

“They can also reduce their energy bills further by shopping around for a better deal. Ofgem will continue to protect consumers in the difficult months ahead as we work with industry and government to build a greener, fairer energy market.”

Ofgem has decided to roll the prepayment meter cap into the default tariff price cap (known as “the price cap”) to ensure these households get the protection they need. The existing prepayment meter cap expires at the end of this year.

Today Ofgem also recommends that the price cap is not lifted at the end of this year and that it should remain in place in 2021 for these households on default tariffs and prepayment meters.

According to the price cap legislation, the price cap can be lifted from 2020 (and no later than 2023) if “the conditions for effective competition” in the domestic retail energy market are in place which would prevent a return to customers on default deals being overcharged for their energy.

From 2020, Ofgem is required to give an annual independent assessment on whether these conditions are in place. The decision on whether to lift the cap rests with the BEIS Secretary of State.

Ofgem’s recommendation is based on its analysis of market features such as customer engagement levels, switching trends, price differentials between tariff types and the quality of customer service provided by suppliers.

Notes

1. In June 2020 Ofgem announced a package of support for prepayment meter customers and those struggling with energy bills. If customers are struggling to pay for energy bills they should contact their energy supplier as soon as possible. Depending on their circumstances, customers may be eligible for extra help with their energy bills or services.

2. The price cap is a cap on a unit of gas and electricity, with standing charges taken into account. It is not a cap on customers’ overall energy bills, which will still rise or fall in line with their energy consumption.

3. The £1,042 per year level of the cap is based on a household with typical consumption on a dual electricity and gas bill paying by direct debit. Customers who pay by standard credit (cash or cheque) pay an additional £79 based on the higher cost for suppliers to serve them. Savings on gas bills for the coming winter period are higher due to the significant reduction in wholesale gas prices. Customers who use only electricity will make savings, but these will be significantly lower overall. Customers will also experience different levels of savings depending on the region they live in.

Breakdown of cap

Note: cost breakdowns above do not add up exactly to total cap levels due to rounding effect.

Data for the graph can be found below:

A one off “wholesale energy adjustment” has been added to the next price cap period. This increases the cap level by around £15 in annualised terms or £10 for the next price cap period after which it will disappear. It does not apply to the prepayment level of the cap which explains why the reduction for the prepayment level is higher for this period. More information. Ofgem has also reduced the allowance for smart meter costs for the next price cap period by £4 following a review. More information.

4. TDCV: The values shown in the text above include VAT, and are expressed for the current Typical Domestic Consumption Values (TDCV) of 2,900kWh of electricity, 12,000kWh of gas, and 4,200kWh of electricity for Economy 7. Ofgem decreased the TDCV on April 1 2020 to reflect decreasing average consumption (previously they were 3,100kWh of electricity, 12,000kWh of gas, and 4,200kWh of electricity for Economy 7). From this date, Ofgem has been using the new TDCVs to express the default tariff price cap and prepayment meter cap in all publications. Previous publications on the levels of the caps will therefore not be exactly the same. Even after stripping out the impact of lower consumption figures, the level of the default tariff cap is still the lowest since it was introduced on January 1 2019.

5. From 1 October the equivalent per unit level of the price cap to the nearest pence for a typical customer paying by direct debit will be 18p per kWh for electricity customers and 3p per kWh for gas customers.

6. Suppliers buy electricity and gas on the wholesale markets in advance, purchasing ‘forward contracts’ gradually over time. The default tariff price reflects suppliers’ costs because we use the wholesale prices of the relevant forward contracts that were sold in advance during an ‘observation window’ before each 6 month price cap period. The observation window for the winter price cap period (October – March) is the previous February - July. The observation window for the summer price cap period (April - September) is the previous August - January. The graphs below show a) how wholesale gas and electricity prices for the relevant contracts on offer in each observation window result in an allowance that reflects suppliers’ average costs:

Data sets behind this graph are proprietary, and can be sourced from ICIS.

Data sets behind this graph are proprietary, and can be sourced from ICIS.

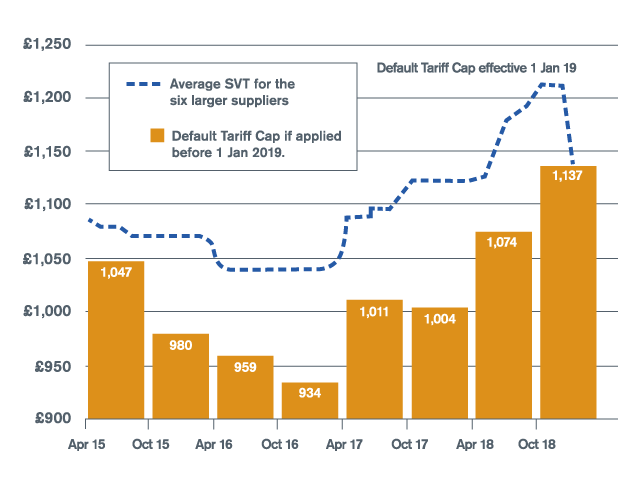

7. Ofgem analysis at the time the default tariff cap was introduced on 1 January 2019 suggests that the default tariff price cap would have reduced the price of the average standard variable tariffs from the six largest suppliers by around £75 to £100 per year since April 2015 had it been in place over this period. The chart below shows these suppliers have consistently charged more than the indicative level of the default tariff cap, which reflects the estimated costs of an efficient supplier. This analysis suggests had the cap not been introduced on 1 January 2019, customers would be paying significantly more. However, it is impossible to estimate an exact savings figure going forward as suppliers can no longer price above the level of the cap.

8. Conditions for Effective Competition: Effective competition in the domestic retail energy market means the absence of significant barriers to consumers being able to access, assess and act on information about the products and services they may want, driving rivalry between firms to win and retain them. Last year Ofgem set out three conditions (see below in italics) that would need to be in place for this to happen:

Ofgem’s conclusion on all three is that these conditions are not yet in place:

- Structural changes from the government, Ofgem and the wider market are facilitating competition. Key market features include the smart meter rollout and Ofgem’s Faster and More Reliable Switching Programme. Progress has been steady, but slower than expected and further limited by the COVID-19 crisis.

- Competition should be expected to work well in the absence of the price cap. Key market features include levels of consumer engagement, and trends in switching. There have been some improvements in these areas, however Ofgem remains concerned about the number of disengaged customers.

- Competition should deliver fair outcomes for consumers. Key market features include price differentials between default tariffs and fixed tariffs and the quality of service across suppliers. It is not clear that customer service is improving sufficiently, or that households on default tariffs would continue to pay a fair price if the cap was lifted.

9. Ofgem decided to roll the prepayment meter cap into the default tariff price cap (known as the “price cap”). This means price protection for prepayment meter customers will continue as long as the price cap is in place. The existing prepayment meter cap expires at the end of 2020.

10. Information and materials for consumers about the price caps is available at: www.ofgem.gov.uk/energy-price-caps

Further Information

For media, contact

Michael Anderson: 0207 901 7079 / Michael.Anderson@ofgem.gov.uk

About Ofgem

Ofgem is the independent energy regulator for Great Britain. Its priority is to make a positive difference for consumers by promoting competition in the energy markets and regulating networks.

For facts, figures and information about Ofgem’s work, see Energy facts and figures or visit the Ofgem Data Portal.

For energy insights and updates straight to your inbox from Ofgem, please subscribe.