Energy prices to fall again this winter

- Publication type:

- Press release

- Publication date:

- Topic:

- Energy pricing rules

- Subtopic:

- Energy price cap

Related links

- Energy price cap (default tariff): 1 October to 31 December 2023

- Amending price cap methodology for Earnings Before Interest and Tax (EBIT) allowance decision

- Decision on technical changes to the price cap methodology

- Allowance for additional support credit bad debt costs

- Levelling the cost of standing charges on prepayment meters

- Reviewing the Consolidated Segmental Statement - our initial proposals

Energy regulator Ofgem has today (Friday, 25 August, 2023) announced a further reduction in the energy price cap for the last quarter of 2023 (Oct to Dec).

The change will bring the average dual-fuel energy bill below £2,000 a year for the first time since April 2022, saving households an average of £151 on the previous quarter.

From 1 October – 31 December, the cap will be set at an annual level of £1,923 for a dual fuel household paying by direct debit based on the current typical domestic consumption values (TDCV) rate.

The drop, the lowest level since October 2021, reflects further falls in wholesale energy prices, as the market stabilises and suppliers return to a healthier financial position after four years of loss making.

Ofgem is clear that it expects all suppliers to continue improving customer service, to support their most vulnerable customers and to shore up their financial resilience to prevent the kind of failures we saw two years ago. Ofgem recognises that there is some excellent best practice across the sector but expects this to be the norm with poor practice stamped out.

Alongside changes to the price cap, Ofgem has also introduced measures to reduce costs for prepayment meter customers and ensure extra support for those facing disconnection from the network.

The price cap savings – which can be passed on more quickly to customers thanks to the price cap updating quarterly – continues the downward trend since prices peaked at £4,279. However, it remains well above the average before the energy crisis took hold in 2021 and the market remains volatile.

Jonathan Brearley, Ofgem CEO, said:

“It is welcome news that the price cap continues to fall, however, we know people are struggling with the wider cost of living challenges and I can’t offer any certainty that things will ease this winter.

“That’s why we’ve introduced new measures to support consumers including reducing costs for those on pre-payment meters, and introducing a PPM code of conduct that all suppliers need to meet before they restart installation of any mandatory PPMs.

“There are signs that the financial outlook for suppliers is stabilising and reasonable profits are returning. With the small additional allowance we’ve made to Earnings Before Interest and Tax (EBIT), this means there should be no excuses for suppliers not to be doing all they can to support their customers this winter, and to reinforce this we’ll be introducing a consumer code of conduct which we will look to have in place by winter. This code will ensure there are clear expectations of supplier behaviours especially for their most vulnerable consumers with whom suppliers should be reaching out proactively, with compassion and understanding. There are great examples of suppliers already doing this but I want to see this become the norm in such an essential sector that has such a big impact on people’s lives.”

Ofgem understands that while suppliers cannot control wholesale prices or fix the wider cost of living pressures hitting their customers, now the market has stabilised, they must continue improving customer service and ensure that support across the board is accessible, responsive and understanding, including giving time to make pay arrangements and directing customers to further support and advice. They must also invest in strengthening their financial resilience to protect consumers against the cost of supplier failure.

Additionally, while still low by pre-crisis levels, we are starting to see more and more competitive fixed deals coming onto the market and levels of switching are slowly increasing.

With a lower price cap and reasonable profits starting to return, there is an opportunity for this to continue to grow. Anyone considering fixing should weigh up all the facts and consider what is most important to them, whether that’s the lowest price, or the certainty of knowing exactly what they will pay each month. It’s important customers are comparing fixed deals with the new, lower price cap announced today. Suppliers are expected to ensure they are transparent in releasing all tariff information to enable consumers to make simple comparisons of the deals available to them across the market.

While the price cap has protected households from the full extent of volatility and surges in wholesale prices over the last two years, it was originally introduced by the Government to protect the minority of consumers who did not switch rather than to cover the vast majority of consumers, as it does now. It is a blunt tool and in the current market it has costs and as well as benefit. It’s important to look at alternative models to examine whether they could work better with the current volatile market and the move to net zero.

Ofgem has also today published:

- A Final Decision to raise the Earnings Before Interest and Tax (EBIT) allowance by £10 per customer per year. Most of this increase is to cover Renewable Obligations ringfencing so that customers’ money is protected in the event of a supplier failure.

- Removal of the temporary RO ringfencing allowance, worth £8 per customer and covered by the additional EBIT costs above

- A new sliding scale for EBIT meaning if prices surge, the EBIT allowance reduces as a percentage preventing suppliers from making excessive cash gains from a high price market

- Final decision on the allowance for additional support credit (ASC) bad debt costs - a new allowance to help ensure some of the most vulnerable consumers remain on supply this winter

- Implementation of UNC840 in the cap, reducing the PPM premium

- Price Cap model technical changes Final Decision

- Levelisation Policy Consultation

By raising the EBIT allowance, Ofgem is taking the next step in its drive to make the retail energy sector more resilient, as we move into another difficult winter when price volatility remains a risk.

At the height of the energy crisis around 30 suppliers failed because they did not have enough capital in the reserve to stay in business – and the cost was shared among all energy consumers, adding £83 to bills.

With suppliers only now starting to recoup a portion of their multi-billion pound losses over the past four years, a small increase in permitted profit margins will allow companies to better cover their costs, attract investment and retain financial stability protecting consumers into the future.

Raising the EBIT allowance from its current rate of 1.9% to 2.4% from 1 October will involve an average £10 increase in bills per year. £8 of this will cover costs to consumers incurred by an additional requirement of suppliers to ringfence enough funds to cover their Renewable Obligations, protecting consumers from additional costs should a supplier go bust.

The EBIT rate, which is well within international norms for energy retail profits and lower than most other business sectors in Britain, will also be altered from a ‘flat rate’ to a more flexible model that tracks the price cap level and tapers as low as 1.75% in the event of another price surge in the wholesale market. This would prevent suppliers from making excessive cash profits in a high-cost market.

Strengthening the commitment to supporting struggling and vulnerable consumers, Ofgem is also reducing the cap for prepayment meter (PPM) customers by £51 per year through an updated approach to calculating the costs of unidentified gas, approved in April this year.

Using some of the benefit from this change, the regulator is now able to introduce an initial 12-month allowance to cover increased debt costs associated with Additional Support Credit that is offered to PPM customers, often at the point of disconnection. This new allowance will help ensure some of the most vulnerable consumers remain on supply this winter.

Longer term, Ofgem seeks to permanently end the PPM premium, where prepayment customers are charged more than those who pay by direct debit to cover the additional costs and resources required by suppliers to provide energy via PPM. A consultation is underway with an aim to ‘levelise’ these standing charges by April 2024 to coincide with the end of government support currently in place via the Energy Price Guarantee.

The next quarterly price cap announcement will be in November 2023, covering January – March 2024.

NOTES TO EDITORS

The energy price cap was introduced by the government and has been in place since January 2019, and Ofgem is required to regularly review the level at which it is set. It ensures that an energy supplier can recoup its efficient costs while making sure customers do not pay a higher amount for their energy than they should. The price cap, as set out in law, does this by setting a maximum that suppliers can charge per unit of energy.

The new price cap figure is calculated against the current Typical Domestic Consumption Values (TDCV) rate, which estimates the average usage of a dual fuel household paying by direct debit. A revised TDCV rate will come into effect from October 1 and will be used for the next price cap period commencing January, 2024.

Ofgem has presented the new price cap figure based on the existing rate to ensure a clearer comparison of prices in relation to the current standard variable tariff.

Earlier this year, Ofgem chief executive Jonathan Brearley wrote to energy suppliers setting out clear expectations on financial resilience and supporting consumers, including the overarching principle that companies must use profits to improve their capital position before paying dividends to shareholders.

The letter also warned that the regulator is closely monitoring levels of customer service, support and financial adequacy – and can, and will, act where suppliers are found lacking.

Part of this monitoring will include checking for undue benefits for suppliers as prices fall and profits return and, where appropriate, Ofgem will recoup money from suppliers for consumers via the price cap. In July, companies were informed via an open letter that the regulator will conduct a review of wholesale energy costs and consider whether allowances for suppliers fairly reflect the actual costs incurred in the period October 2022 to September 2023.

If this review finds that allowances excessively benefited suppliers as prices fell in 2023, the money will be delivered back to consumers via adjustments to the January 2024 price cap. In short, unreasonable profits can be clawed back.

Ofgem has robust rules in place to help people in vulnerable situations, and suppliers are obliged to offer payment plans and direct customers to available support.

The regulator has made it clear to suppliers that improving customer service standards must be a priority, as outlined the recent Statutory Consultation on Consumer Standards.

Ofgem has already taken action against suppliers this year for unacceptable standards in call waiting times and for failing to provide compensation for delayed final bills for customers when switching.

The EBIT allowance increase is part of a package of measures to create a more resilient and investable supply sector. This will ultimately benefit consumers, as it protects them from the cost of supplier failures and enables investment to improve the quality of services.

Ofgem believes the increase is necessary to allow the sector to attract investment and help towards achieving improved financial resilience. Beyond that, changes to the way the allowance scales with the overall price cap level means consumers are better protected in the event of a price surge in the future.

Bill-payers will continue to receive additional support via the EPG until the end of March 2024, as confirmed by the Chancellor on Thursday, 17 November, 2022. The level of this support is set by Government.

Updated number of customers on different tariff types as of July* 2023

- New no. of customers on SVTs – ‘around 29 million’

- New no. of SVT (non-PPM) customers – ‘around 25 million’

- New no. of SVT PPM customers – ‘around 4 million’

- Total number of customers on fixed tariffs: 'around 3 million' (with the vast majority being non-PPM)

*Latest Financial Responsibility RFI data is for July 23. Tariff and Customer Account RFI data is as of July 23 (used to calculate the SVT payment method splits)

The tariff cap was legislated by government in order to protect default tariff customers (i.e. those on standard tariffs) from being overcharged. Price cap updates are currently published on a quarterly basis. More information on this can be found on the "Ofgem confirms changes to the price cap methodology and frequency ahead of new rate to be announced later this month" press release.

The price cap level is based on typical use for an average household and is a cap on energy unit price not a cap on total bills. For an individual customer, the amount they will pay varies depending on how much energy they use, where they live, and how they pay for their energy.

The methodology for setting the price cap is set out here and is regularly reviewed by Ofgem:

Default tariff cap: decision - overview | Ofgem

Price cap - Decision on changes to the wholesale methodology | Ofgem

The price cap protects around 29 million customers on default or variable rates. The £1,923 per year level of the cap is based on a household with typical consumption on a dual fuel electricity and gas bill paying by direct debit.

For customers who pay by standard credit (cash or cheque), the default cap has decreased by £159 from £2,211 to £2,052 for typical dual fuel consumption. The additional costs reflect the higher cost for energy companies to serve them.

The 29 million customers protected by the price cap includes around 4 million prepayment meter (PPM) customers. The PPM level of the default cap has decreased by £128 from £2,077 to £1,949 for average dual fuel consumption. The additional costs for PPM customers reflects the higher cost for energy companies to serve them. For electricity only customers on Economy 7 paying by Direct Debit has decreased by £102 from £1,400 to £1,298 for typical consumption (4,200 kWh).

The values shown in the text above include VAT and are expressed for the current Typical Domestic Consumption Values (TDCV) of 2,900kWh of electricity, 12,000kWh of gas, and 4,200kWh of electricity for Economy 7.

We will be changing how we communicate typical bills from 1 Oct 2023, in line with our Decision on Typical Domestic Consumption Values. From 1 Oct price cap levels and typical bills will be expressed in 2023 TDCV of 2,700 kwh of electricity, 11,500 kWh of gas and 3,900 kWh of electricity for Economy 7. In the interests of transparency, we have compared what the July – Sept 2023 and the Oct – Dec 2023 cap levels announced today would be using 2023 TDCVs.

The price cap is a cap on a unit of gas and electricity, with standing charges taken into account. It is not a cap on customers’ overall energy bills, which will still rise or fall in line with their energy consumption. From 1 October the equivalent per unit level of the price cap to the nearest pence for a typical customer paying by direct debit will be 27.35p per kWh for electricity customers and a standing charge of 53.37p per day. The equivalent per unit level for a typical electricity muti-register customer is 26.26p per kWh and with a standing charge of 53.36p per day. The equivalent per unit level for a typical gas customer is 6.89p per kWh with a standing charge of 29.62p per day.

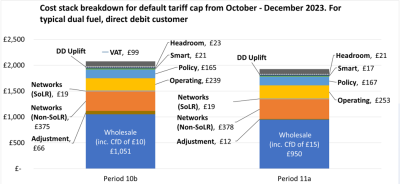

Breakdown of costs in the energy price cap

Dual fuel customer paying by direct debit, typical energy use (GB £) £1,923

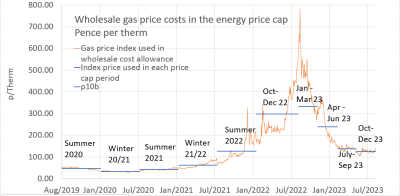

Wholesale gas price costs in the energy price cap

The chart above shows indexed wholesale prices for Gas to Period 11a (October – December 2023).

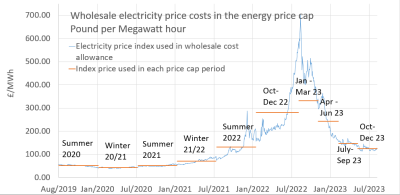

Wholesale electricity price costs in the energy price cap

The chart above shows indexed wholesale prices for Electricity to Period 11a (October – December 2023).

Data sets behind these graphs are proprietary and can be sourced from ICIS.

Related links

- Energy price cap (default tariff): 1 October to 31 December 2023

- Amending price cap methodology for Earnings Before Interest and Tax (EBIT) allowance decision

- Decision on technical changes to the price cap methodology

- Allowance for additional support credit bad debt costs

- Levelling the cost of standing charges on prepayment meters

- Reviewing the Consolidated Segmental Statement - our initial proposals